A little known moment in US fiscal history finally comes to light today at 1898 Revenues. As the title of this post indicates, President Theodore Roosevelt, the first great conservationist President, considered extending certain Spanish-American War taxes in order to support and expand his goal of preserving some of America United States were placed under public protection by Roosevelt . And the President considered how these great reserves would be cared for, and in turn, how that care would be supported.

Practically, Roosevelt wondered whether the American public would tolerate new taxes or fees to cover what was, at the time, a radical concept. Preservation of natural wonders was not something the common man considered a public priority. So Roosevelt considered whether a minor extension of existing taxes set to expire would be little noticed and accepted.

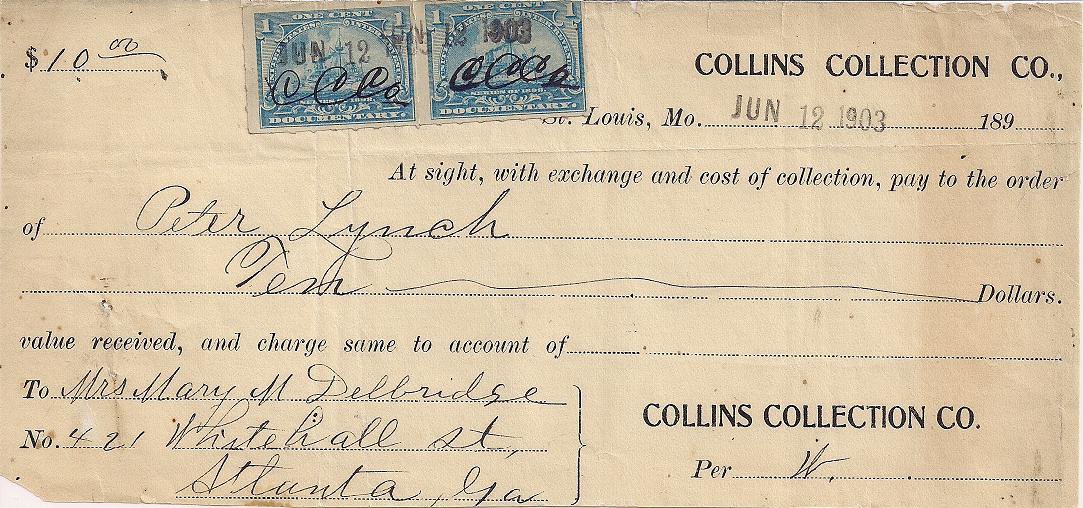

Realizing that the Spanish-American War taxes on checks and drafts were to expire at the end of June, 1901, Roosevelt proposed to some of his trusted advisors whether a one-year extension of the check tax (2 cents per check) could raise the revenue necessary to support to National Parks programming through the end of his term.

In a short time, John W. Yerkes, Roosevelt's Commissioner of Internal Revenue had done the calculations and assured Roosevelt that not only would the revenue be sufficient for expected costs of the national parks, but would far exceed the needs. Roosevelt then devised a strategy to make these "new" yet old taxes acceptable to the American Public.

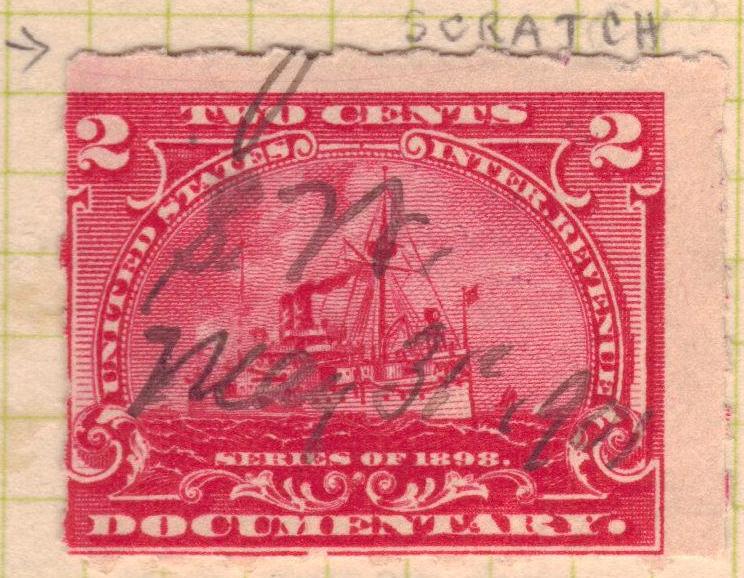

Looking over a 2 cent battleship documentary stamp while at his home at Sagamore Hill, New York, Roosevelt took it upon himself to create a redesign. If the check tax was to be extended to make the tax seem as non-intrusive as possible, why not make a subtle change to the existing tax stamp, one more in-line with the ruggedness and the spirit of park preservation? Just as private die proprietary users like Johnson and Johnson made subtle changes to the battleship design, Roosevelt thought that the replacement of the battleship with a canoe, the well known water craft of the rugged and self-reliant American Indian, would make a perfect center for a new stamp.

Four water colors of canoes were on the wall of his study at Sagamore Hill, and Roosevelt took his inspiration from one of these. Carefully scraping away the battleship off the stamp with a new razor blade, Roosevelt created a blank center in the stamp for which to draw his own vessel.

One canoe was chosen for the design, much like the single battleship in the original stamp. Roosevelt used a fountain pen and placed a canoe on the waves, with two native -Americans with paddles in the canoe. He then sketched in mountain outlines above their heads.

Once back in Washington, Roosevelt took the stamp design to Yerkes to be considered for engraving and actual use. John Yerkes liked the design, but while Roosevelt was in New York, Yerkes began to look into whether general revenues might cover Roosevelt's new and growing parks program. After consultations with the Secretary of the Treasury Lyman J. Gage, Yerkes and Gage agreed that an extension of the check tax would be unnecessary. This would make Roosevelt's search for revenue much simpler. Yerkes promptly told Roosevelt of the lack of a need for a tax extension, and the matter, and the stamp above, were soon forgotten.

Looking back on this little known moment in philatelic history, it is amazing that this stamp and story have survived. But Roosevelt family members preserved the stamp and the legend, and 1898 Revenues is proud to finally tell the story.

BTW: Roosevelt would often place hidden messages in his letters, often by coding them in the first letter of each paragraph. 1898 Revenues uses the trick on occasion.

Practically, Roosevelt wondered whether the American public would tolerate new taxes or fees to cover what was, at the time, a radical concept. Preservation of natural wonders was not something the common man considered a public priority. So Roosevelt considered whether a minor extension of existing taxes set to expire would be little noticed and accepted.

Realizing that the Spanish-American War taxes on checks and drafts were to expire at the end of June, 1901, Roosevelt proposed to some of his trusted advisors whether a one-year extension of the check tax (2 cents per check) could raise the revenue necessary to support to National Parks programming through the end of his term.

In a short time, John W. Yerkes, Roosevelt's Commissioner of Internal Revenue had done the calculations and assured Roosevelt that not only would the revenue be sufficient for expected costs of the national parks, but would far exceed the needs. Roosevelt then devised a strategy to make these "new" yet old taxes acceptable to the American Public.

Looking over a 2 cent battleship documentary stamp while at his home at Sagamore Hill, New York, Roosevelt took it upon himself to create a redesign. If the check tax was to be extended to make the tax seem as non-intrusive as possible, why not make a subtle change to the existing tax stamp, one more in-line with the ruggedness and the spirit of park preservation? Just as private die proprietary users like Johnson and Johnson made subtle changes to the battleship design, Roosevelt thought that the replacement of the battleship with a canoe, the well known water craft of the rugged and self-reliant American Indian, would make a perfect center for a new stamp.

Roosevelt at the stand-up desk in his study at Sagamore Hill. The design for the stamp below was created by Roosevelt at this desk.

Four water colors of canoes were on the wall of his study at Sagamore Hill, and Roosevelt took his inspiration from one of these. Carefully scraping away the battleship off the stamp with a new razor blade, Roosevelt created a blank center in the stamp for which to draw his own vessel.

The Roosevelt designed "Canoe" check tax stamp. This is the actual stamp created by Roosevelt at Sagamore Hill.

One canoe was chosen for the design, much like the single battleship in the original stamp. Roosevelt used a fountain pen and placed a canoe on the waves, with two native -Americans with paddles in the canoe. He then sketched in mountain outlines above their heads.

Once back in Washington, Roosevelt took the stamp design to Yerkes to be considered for engraving and actual use. John Yerkes liked the design, but while Roosevelt was in New York, Yerkes began to look into whether general revenues might cover Roosevelt's new and growing parks program. After consultations with the Secretary of the Treasury Lyman J. Gage, Yerkes and Gage agreed that an extension of the check tax would be unnecessary. This would make Roosevelt's search for revenue much simpler. Yerkes promptly told Roosevelt of the lack of a need for a tax extension, and the matter, and the stamp above, were soon forgotten.

Looking back on this little known moment in philatelic history, it is amazing that this stamp and story have survived. But Roosevelt family members preserved the stamp and the legend, and 1898 Revenues is proud to finally tell the story.

BTW: Roosevelt would often place hidden messages in his letters, often by coding them in the first letter of each paragraph. 1898 Revenues uses the trick on occasion.